Three Possible 2021 Outcomes: Pick Only One

This article appeared in Electronic Design and has been published here with permission.

What you’ll learn:

- The impacts of COVID-19 and China’s semiconductor push on the health of the chip market.

- Three very different ways that the market could evolve.

Semiconductor industry revenue forecasts are usually pretty easy to get right. For most of its history, the industry has undergone highly predictable cycles, enjoying high profits whenever there’s a shortage and suffering from profitless oversupplies when its own capital-spending binges create excess production capacity. This dynamic plays out predictably when the economy is stable, but every so often some external event causes a dramatic enough change that it causes the market to undergo a surge or a collapse.

In the past, such events occurred no more often than once every 15 years or so: 1971, 1986, then 2001. Recently, though, they have been more frequent, with the Global Financial Collapse hitting semiconductors in 2009 and the U.S.-China Trade War causing important shortages in 2018.

So far, the COVID-19 pandemic has boosted, rather than harmed, chip revenues. Most prognosticators feared that the 2020 semiconductor market would suffer as a result, since consumer purchases dropped early in the year. However, the loss in the consumer sector was more than offset by increased purchases to support work-from-home and home schooling, and significant increases in online gaming, online shopping, and streaming video consumption.

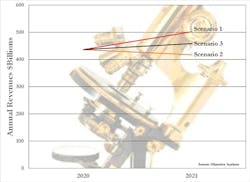

As we look to 2021, we must consider whether the industry will behave relatively normally, as it did in 2020, or whether it will be severely impacted by either of two very likely scenarios: A COVID-driven global financial collapse, or a sudden surge of chips from new suppliers in China. While I’m unable to tell which of these routes the market will take, it’s not that difficult to predict how revenues will fare in each scenario. Let’s have a look at each.

Scenario 1: Healthy Market

Our first scenario guesses that 2021’s chip market will suffer no greater impact from the ongoing COVID-19 pandemic than it did in 2020. Last year’s market statistics haven’t yet been reported, but it appears likely that revenues will show 6% growth. Can we expect similar growth in 2021? In this “best-case” scenario, 6% growth is perhaps even low. Growth in 2021 could even exceed 15%!

This outcome will occur if prices are stable and unit demand growth continues along at its current pace. The second of these is nearly guaranteed. Almost nothing ever impacts demand growth, and even if it does, the change is always temporary and compensated for later on. Price is the factor that causes semiconductor market swings. As a general rule, prices are stable when past capital spending (CapEx) has been low, and they fall when excessive capital spending leads to an overage.

Capital spending has been low enough for the past few years to prevent the emergence of an overcapacity in 2021. Foundries like GLOBALFOUNDRIES, Samsung, TSMC, and UMC, along with several smaller competitors, have already reported capacity shortages, and leading IDMs are experiencing either tightness or a healthy supply/demand balance. Since CapEx in 2019 didn’t spike over that of 2018, it seems that this situation could continue as long as the other external factors listed below don’t detract from the market.

The semiconductor market is legendary for its revenue swings, but a deeper dive into the figures shows that almost all of the market’s mood swings occur in the commodity memory businesses. The largest of these are DRAM and NAND flash. These chips’ share of total semiconductor revenues usually varies between 20% and 30%, depending on whether they’re selling at a profit or a loss.

The Objective Analysis semiconductor forecast is built on an understanding of this phenomenon, and this has led us to have the most consistently accurate forecast in the semiconductor industry. This forecast calls for solid 2021 growth provided the global economy is stable, and provided that important new sources don’t develop over the course of the year.

Scenario 2: Global Financial Collapse

A second natural scenario guesses that the current COVID-19 pandemic might cause an economic meltdown similar to the Global Financial Collapse of 2008-9.

While I’m not an economist, I do see certain very worrying trends: Services are faring very poorly, with everything from airlines and hotels through theaters and restaurants closing their doors. This is due to restrictions that prevent them from conducting their normal line of business and to customers who are afraid to participate in innocent events that could prove unhealthy or even lethal.

The difficulties endured by both of these businesses and their employees have reduced tax revenues. At the same time, governments are issuing monetary incentives to try to bolster their countries’ economies, which is leading to ballooning government deficits.

I don’t have a good idea of how much of this the economy can endure before facing a collapse, but I worry that such an event is very possible.

What I can predict with some confidence is how the semiconductor market is likely to fare should such a collapse occur. During this kind of event, the prices of commodity semiconductors fall to cost, but unit demand tends to maintain stable growth. There’s usually a momentary demand lull that’s soon offset by pent-up demand, with the result that the year’s unit consumption follows a predictable path.

How far can prices fall? The two biggest commodities in the semiconductor market are DRAM and NAND flash. DRAM margins are currently over 40%, while NAND flash chip margins average around 10%. This means that, in the event of a collapse, DRAM prices would fall 40% and NAND flash prices by 10%. If we crank these numbers into the same semiconductor forecast used above, we arrive at a revenue decline of up to 4.5%, depending on the actual timing of the collapse: The later the collapse, the smaller its impact on the year’s revenues. It’s a sliding scale.

Scenario 3: China Comes on Line

Since 2015, China’s government has been pushing to make its contract manufacturing and other electronic businesses less dependent on externally supplied semiconductors. The Made in China 2025 initiative has amassed a fund of over $100 billion to develop production facilities that would provide Chinese memory chip users a good share of their requirements.

Memories have been chosen since they are commodities: All memory chip makers’ DRAM and NAND flash chips behave the same, so a new supplier can take market share from established players simply by offering a similar chip at a better price. (This is all explained in great detail in the Objective Analysis report titled “China’s Memory Ambitions.”)

These efforts aren’t progressing as well as had been hoped. China’s major NAND flash maker, YMTC, has been shipping small volumes of product for over a year, but it’s far from becoming the mainstream supplier that it had hoped for by 2020. The country’s DRAM players are even farther behind.

For the past few years, Objective Analysis has projected that China’s memory companies would abandon their efforts to produce an internally developed technology in 2020 and would sign technology agreements with leading memory chip vendors within 2020 to become important suppliers in 2021. Those agreements have yet to be announced, delaying these manufacturers’ rise to prominence in the market.

In similar past situations, memory makers have exploded onto the market within a quarter or two of signing such agreements. This means that there’s still time for at least YMTC to become a significant source of NAND flash chips. The DRAM suppliers are likely to take longer.

Once these companies start to make a meaningful contribution to the market, an oversupply will develop, causing prices to fall to cost. As with Scenario 2, NAND prices would fall by about 10% and DRAM prices by over 40%. Since these are supplied by different companies that are at different stages of tooling, the timing of a DRAM collapse will be later than the NAND flash price collapse.

The earliest that a NAND flash price collapse could begin is the second half of 2021. At the very earliest, a DRAM collapse would occur in the fourth quarter.

If we plug this into the same forecast, then our worst-case outcome for an aggressive ramp up of China production without a pandemic-driven collapse would still result in growth over 5%, once again depending on the timing of the price fall. The later that China’s suppliers rise to prominence, the weaker their impact on pricing.

Wrap Up: Choose One

This gives us three possibilities:

- The economy stays healthy, China’s producers remain in the background, and the semiconductor market grows as much as 15%.

- The COVID-19 pandemic causes a global financial collapse that, depending on its timing, could cause the semiconductor market to decline by as much as 4.5%, depending on when in the year that global financial collapse occurs.

- COVID causes no impact, but China’s memory chip producers enter the market to create an oversupply, muting growth to a maximum of 5%.

For the time being, Objective Analysis is projecting the first scenario, but with ample concerns that the pandemic will create a collapse that we’re unable to forecast. This is a more difficult year to predict than years with clear health in the economy.

We’re advising our clients to plan for growth, but to constantly watch out for signs of weakness in the global economy. Successful companies will have a plan for both scenarios.

References

Objective Analysis forecast accuracy page; https://Objective-Analysis.com/forecast-accuracy/

Smartkarma: Forecasting the Semiconductor Market; https://www.smartkarma.com/insights/forecasting-the-semiconductor-market

Objective Analysis report: China’s Memory Ambitions; https://Objective-Analysis.com/reports/#China

About the Author

Jim Handy

Analyst, Objective Analysis

Jim Handy, a widely recognized semiconductor analyst, comes to Objective Analysis with over 30 years in the electronics industry including 14 years as an industry analyst for Dataquest (now Gartner) and Semico Research.

His background includes marketing and design positions at market-leading suppliers including Intel, National Semiconductor, and Infineon.